Your Step-By-Step Guide to Investing an RRSP Into a GIA

If you’re at all familiar with a GIC you’d get at the bank, you already understand one of the biggest reasons why you might invest your RRSP into a GIA: that it comes with little to no risk.

First things first, what’s a GIA?

Short for Guaranteed Interest Annuity, a GIA is a low-risk investment vehicle offered by insurance providers. It gives Canadians the opportunity to invest their money a little differently than they would at a bank.

At Serenia Life, we offer two very different annuity products for two very different purposes:

- Guaranteed Interest Annuity (GIA) allows you to park your money in a low-risk investment, and is best for short- or long-term goals.

- Single Premium Annuity (SPA) lets you turn your hard-earned income into a guaranteed monthly pay cheque, which can be perfect for funding your retirement years.

While a GIA gives you the opportunity to accumulate money for a goal – like a new car, home renovations, a dream vacation, or even retirement – an SPA can turn a lump sum of money into a guaranteed stream of income, typically used when you are no longer working.

Today, we’ll be focusing on the GIA (a.k.a., the insurance version of a GIC), and how you can use it as a means to save for retirement.

Check out Serenia Life’s GIA rates.

Benefits of investing an RRSP into a GIA

If you’re at all familiar with a GIC you’d get at the bank, you already understand one of the biggest reasons why you might invest your RRSP into a GIA: that it comes with little to no risk.

1. Safe investment

That’s right, a GIA might just be the safest investment out there. Which means you don’t have to worry about losing your earnings every time a new tariff is announced – and you don’t have to claim your interest during tax season. That’s because:

-

- You’ll get a guaranteed interest rate for a set term (e.g., 1, 3, or 5 years)

- Your original deposit is protected – meaning, it will never decrease in value even if markets take a nosedive

- You won’t be taxed on your earnings until you withdraw years down the line, at which point you’ll likely be in a lower tax bracket

But there are more reasons to go this route when putting your money in an RRSP – so keep reading!

2. Flexible payout options

Many GIAs are designed to work seamlessly as you transition from a regular salary to retirement income. Here’s how:

- GIAs can be structured to transition smoothly into retirement income via annuity options, like an SPA, or regular payouts.

- This can align nicely with converting an RRSP to a RRIF or annuity at retirement – giving you more control over how and when you access your savings.

3. Personalized service

Let’s face it — when it comes to your money and your future, a little personalized advice goes a long way. The great thing about GIAs is that they’re often sold through licensed insurance brokers . Here’s why that’s a good thing:

- Because they work with multiple insurance providers, they may provide more tailored estate planning and retirement advice compared to representatives at the bank (who can really only sell their bank’s one product).

- Brokers aren’t loyal to one institution so they will seek out the product that is best for you and your goals.

4. Creditor protection

Here’s a benefit you won’t get from the bank: protection from creditors1. If you ever face financial trouble, like a lawsuit or business debt, creditor protection can help keep certain assets safe. Here’s how it works:

- In many provinces, GIAs within insurance contracts may be protected from creditors, especially if a family member is the named beneficiary.

- This is a great option for self-employed individuals or business owners because it helps safeguard your personal assets from any business-related financial risks.

5. Estate planning & probate bypass

Unfortunately, this is a benefit you won’t live to see for yourself – but your loved ones will appreciate it once you’re gone. Here’s why:

Unfortunately, this is a benefit you won’t live to see for yourself – but your loved ones will appreciate it once you’re gone. Here’s why:

- You can name loved ones as beneficiaries to a GIA inside an RRSP.

- This means the funds bypass probate, allowing for faster payout, lower legal fees, and more privacy.

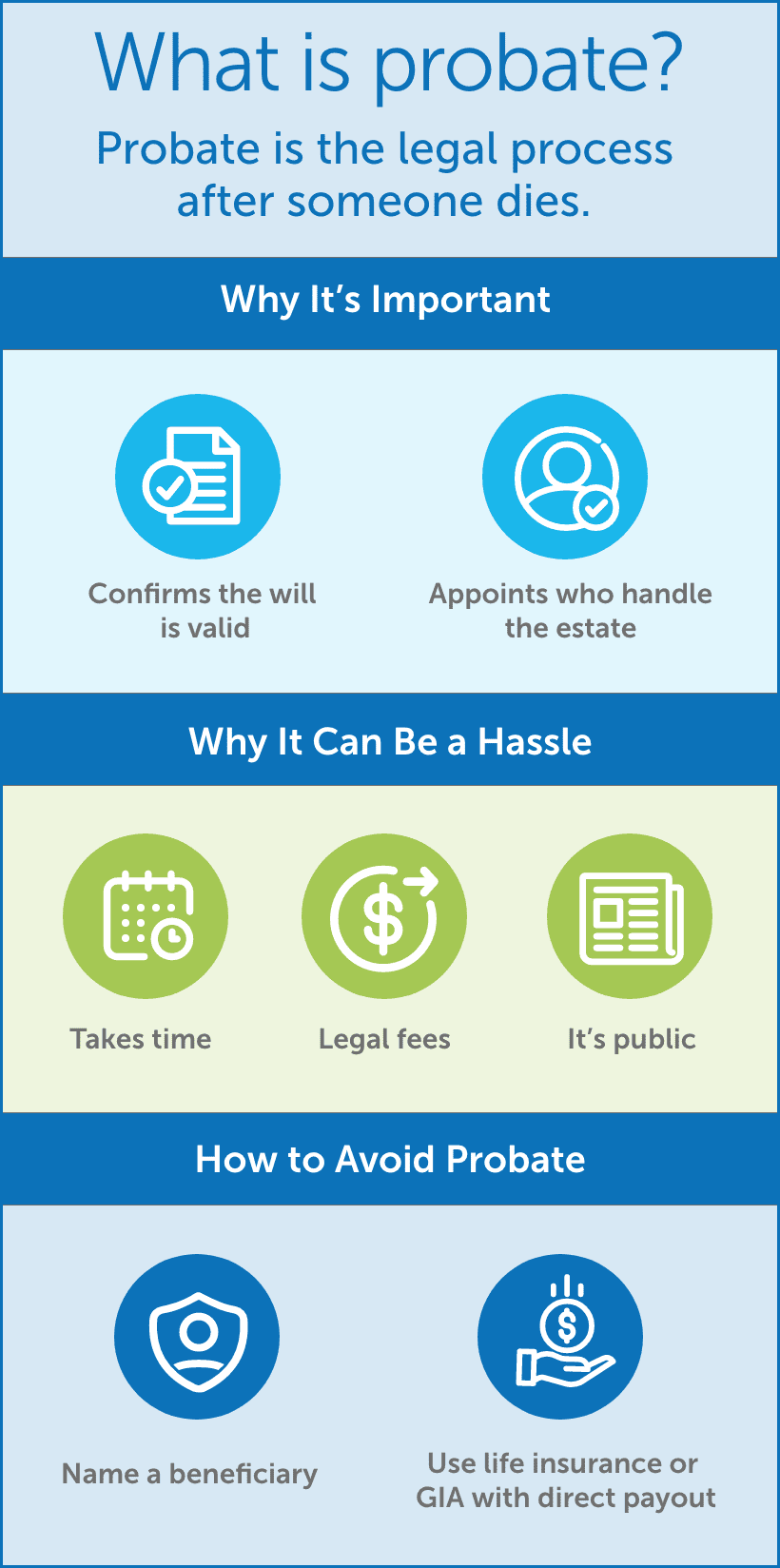

What is probate?

Probate is a legal process where the court must confirm whether the will of a person who has died is valid, and appoints someone to handle their estate. Probate can take weeks or months, and often comes with expensive legal fees and delays.

GIA vs GIC – What’s the difference?

While there isn’t a huge difference between a GIA and a registered GIC, the biggest difference overall is the creditor protection that comes with the “insurance version” of this low-risk investment. Not to mention, when you invest in a Serenia Life GIA, you can count on consistently great rates – that are typically better than those you would find at the bank (source).

But let’s break things down even further…

| GIA (Guaranteed Interest Annuity) | GIC (Guaranteed Investment Certificate) | |

|---|---|---|

| Offered by | Life insurance companies | Banks, credit unions |

| Guarantees | Guaranteed principal & interest | Guaranteed principal & interest |

| Eligible for RRSP | ✅ Yes | ✅ Yes |

| Tax Treatment | Same as RRSP rules | Same as RRSP rules |

| Named Beneficiaries | ✅ Yes (even inside RRSP) | ✅ Yes (only for registered GICs) |

| Payout Flexibility | ✅ Can request lump sum or convert to income stream or annuity | ✅ Can request lump sum or re-invest in GIC |

| Bypasses probate | ✅ With named beneficiary | ✅ Only for registered GICs ❌ Non-registered GICs pass through estate |

| Creditor protection | ✅ Often available | ❌ Not usually protected |

How to grow your RRSP safely with a Serenia Life GIA

Here’s a simplified, step-by-step guide for how to place your RRSP into a Guaranteed Interest Annuity (GIA) with Serenia Life. Download the guide.

| Step 1: Connect with a Serenia Life advisor Set up a meeting, reach out to an advisor near you, or fill out the form below to request a callback. 💬 Tip: Ask for help opening an RRSP and investing it in a Guaranteed Interest Annuity (GIA). |

| Step 2: Open an RRSP If you don’t already have one, your Serenia Life advisor will help you open a Registered Retirement Savings Plan (RRSP). Not to worry – there are no fees to open an RRSP and your contributions are tax-deductible. And, of course, your money will grow tax-free while it’s invested. ✨ You know what they say, good news comes in threes! |

| Step 3: Choose Your GIA’s term length With your RRSP open, it’s time to decide how you want to invest your savings. We’ve already discussed the benefits of selecting a GIA, but there are a few more decisions you’ll need to make with the help of a professional. 📞Your advisor is there to help you pick the term length and explain the interest rates available. |

| Step 4: Transfer RRSP funds (if required) If you already have RRSPs elsewhere (like at a bank), your advisor can help transfer those funds into your new Serenia Life RRSP. This is done using a Transfer Authorization for Registered & Non-Registered Investments form (SER012). 💡 It’s tax-free when done correctly between institutions — so no worries about penalties. |

| Step 5: Sign the paperwork Once everything is set, you’ll sign any necessary documents and your RRSP funds will be placed into the GIA – locking in your guaranteed interest rate. 🎉 Done! Your money is now earning safe, steady returns within your RRSP. |

| Step 6: Keep in touch you can re-invest, switch strategies, or plan your RRSP-to-retirement-income transition (like converting to a RRIF or SPA.) 💰Learn more about setting up an income stream for retirement with a Single Premium Annuity. |

Why choose a Serenia Life GIA for your RRSP?

As a member-based organization whose roots go back nearly 100 years, we encourage kindness by sharing our profits through community outreach, fundraising, and unique member benefits that help Canadians support their family, their community, and the causes they care about. The more we grow, the more we can give.

We provide members with access to a growing collection of member benefits that make a positive impact on their lives and the lives of others. Benefits, such as:

- $2,500 post-secondary scholarships

- Up to $600 towards a fundraiser, and up to $400 to cover volunteer-related expenses in Canada

- Financial support when you hire a lawyer to draft or update your will

- And much more!

View a full list of our member benefits.

Let us help guide you in choosing a GIA vs. GIC when investing in an RRSP

Whether retirement is just around the corner or decades away, putting money away for your golden years is an important part of your overall financial plan. If you’d like to invest your money in one of the safest possible ways, you’re in the right place! Fill out the form below and a Serenia Life advisor will be in touch to answer any questions you might have and set you up for the future.

Disclaimers

1Creditor protection may apply depending on the province, contract structure, and beneficiary designation. Speak to a licensed advisor or legal professional for details.

{kind=link}

{kind=link}

{kind=link}

{kind=link}