Term Life Vs. Whole Life Insurance: Which One Is Right For Me?

Choosing the right life insurance policy can be overwhelming, especially with so many options available in the market. Two common types of life insurance policies in Canada are term life insurance and whole life insurance. Let's compare them in this article...

If you’re finding yourself worried about your financial well-being, you may be surprised to learn how important it is to have life insurance as part of your financial plan. Not only will it ensure that your loved ones are taken care of in the event of your death, but the right policy can even act as investment that you can dip into over your lifetime. But when it comes to term life insurance vs. whole life insurance, how do you choose?

Choosing the right life insurance policy can be overwhelming, especially with so many options available in the market. In this article, we’ll be talking about:

- the difference between term life versus whole life insurance

- the pros and cons of both term life and whole life insurance

- what you should consider when comparing term life versus whole life

Term life insurance

Term life insurance is a straightforward and affordable life insurance policy that provides coverage for a specific term. The typical time periods offered by most carriers are ten years (term 10 life insurance), 20 years (term 20 life insurance), and 30 years (term 30 life insurance).

As a policyholder, you would make regular payments to the insurance company, and in return, your beneficiaries (i.e., the person(s) you choose to receive your life insurance payment in the event of your death) will receive a sum of money called the death benefit if you were to pass away during the selected term.

Once the policy term ends, the coverage ends – which means you would need to renew or purchase a new policy if you still require coverage.

Pros of Term Insurance Versus Whole Life |

|---|

1. Affordable |

2. Customizable |

3. Simple |

Have a family? Here are the top reasons to consider family term life insurance.

Cons of Term Insurance Versus Whole Life |

|---|

1. No opportunity for growth |

2. No lifelong coverage |

Whole life insurance

Whole life insurance is a permanent life insurance policy that provides coverage for your entire lifetime, as long as you continue to make your payments. The policy also has the potential to earn dividends1 that can be used in different ways. For example, they can be used to:

- buy an additional layer of life insurance

- earn more interest on your earnings

- withdraw your money as cash

Not to mention, whole life policies also come with a cash value2 component that can be:

- borrowed to help pay for life events (e.g., tuition fees, wedding, down payment on a home)

- used to make policy payments while the policyholder is still alive

Pros of Whole Life Versus Term Life Insurance |

|---|

1. Lifelong coverage |

2. Investment component |

3. Tax advantages |

Cons of Whole Life Versus Term Life Insurance | |

|---|---|

1. Expensive | |

2. Complex | |

3. Limited investment options |

Comparing term life versus whole life insurance

When comparing term life versus whole life insurance, it’s essential to consider your short- and long-term needs, as well as your financial situation. Here are some key factors to think about:

Key Factors When Comparing |

|---|

Cost |

Coverage |

Growth |

Flexibility |

Case Studies: Meet John and Maria

John’s Story

John is a 35-year-old high school teacher. He and his wife recently had their second child and moved into a home with a bit more space and backyard for the kids to play. After seeing how much their household salary was reduced to after two consecutive maternity leaves, John saw a very real need for life insurance as income replacement should he or his wife die too soon.

After speaking with his advisor, here’s what he got:

- Type: Term 20 – to cover his mortgage while his children are still dependents

- Amount: $1 million – since the recommended amount is 10 x a person’s salary

- Cost: $54 / month – this is for a non-smoking 35-year-old male

Maria’s Story

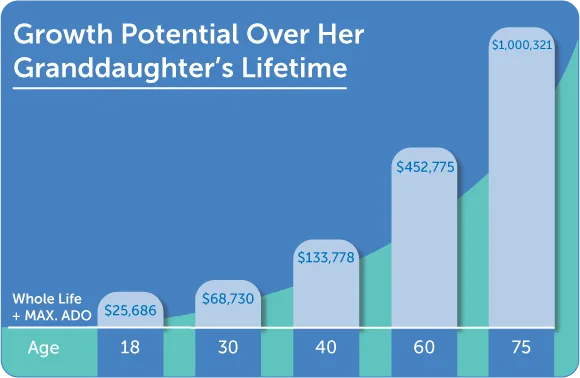

At 55, Maria is a first-time grandmother looking to set up the newest addition to the family with a strong financial foundation. With her mortgage paid off and retirement on the horizon, Maria was able to budget about $100 a month towards her granddaughter’s future. After speaking with her advisor, here’s what she went with:

- Type: Whole Life – which means her granddaughter will be covered for life, despite any future health diagnoses; this policy comes with an investment component that relies on compound interest (via the Additional Deposit Option) for much faster growth

- Amount: $75,000

- Cost: $105.07/ month – this is for a female non-smoker, age 0, and includes: Basic Coverage ($47.70) + maximum Additional Deposit Option ($53.12) + the Guaranteed Insurability of $75,000 Option ($4.25)

So, which is it? Is term life or whole life better for me?

When comparing term life versus whole life insurance, it ultimately comes down to your individual needs and budget. If you are looking for affordable coverage for a limited period, term life insurance may be the best option for you. However, if you want lifelong coverage and the ability to build up your savings over time, whole life insurance may be a better choice. It is important to weigh the pros and cons of each policy type and consult with an expert before deciding. Ready to get the balling rolling? Fill out the form below and we’ll connect you with a Serenia Life advisor.

Frequently Asked Questions

When is term better than whole life insurance?

Term life insurance is usually a better fit when you only need coverage for a specific period — like while you’re paying off a mortgage, raising your kids into independent adults, or covering family income until retirement. It’s typically more affordable than whole life insurance, which makes it a great option if you’re looking for straightforward protection without the long-term commitment or higher cost.

When might whole life insurance not work for you?

Whole life insurance isn’t for everyone. Because it provides lifelong coverage and builds cash value, the cost is higher. If your budget is tight, or you only need coverage for a set time (say, until your kids are independent), term insurance might make more sense.

Can I convert term to whole life later?

Yes — most term policies in Canada let you convert to a whole life policy without having to take a medical exam. This can be a great option if your needs or finances change down the road and you decide you want coverage for life.

Can you have both a term and whole life policy?

Absolutely. Many people do! For example, you might have a smaller whole life policy for permanent protection, and a larger term policy to cover temporary needs, like a mortgage or for your child-raising years. It’s a flexible way to balance cost and coverage.

What happens if I miss a premium payment?

If you miss a payment, most insurers offer a grace period (usually 30 days) to catch up. If you’re still within that window, your coverage stays in place. For whole life policies, if you’ve built up the cash value, your insurer might even use that value to cover missed payments temporarily.

Does whole life always outperform investments?

Not necessarily. Whole life insurance is designed to grow steadily and predictably — not to compete with higher-risk investments like stocks or mutual funds. Its main strength is stability, not high returns. It’s best viewed as part of a balanced financial plan, not a replacement for other investments.

Are dividends guaranteed?

No, dividends on participating whole life policies are not guaranteed. They’re based on the insurer’s performance, including things like investment returns and expenses. However, some insurers (like Serenia Life) have strong dividend track records, which can make payouts fairly consistent over time.

How do you borrow against a whole life policy?

Once your policy builds enough cash value, you can take out a loan from the insurer, using your policy as collateral. There’s no credit check, and you can use the money for anything — like covering business expenses or personal needs. Just remember: Any unpaid loan balance (plus interest) will reduce your death benefit if it’s not repaid.

Disclaimers

1Dividends are not guaranteed and are paid based on the overall experience of Serenia Life Financial, considering all risk factors. Dividends may be subject to taxation. Dividends will vary based on the actual investment returns in the participating account as well as mortality, expenses, taxes, lapses, withdrawals, and other experience of the participating block of policies. These factors have the potential to increase the value of your policy above the guaranteed amount, depending on the dividend option selected.

²Cash values are accessible via a withdrawal, policy loan, or surrender. These may be subject to taxation and a tax slip may be issued. Accessing the policy’s cash value will reduce the available cash surrender value and death benefit.

{kind=link}

{kind=link}

{kind=link}

{kind=link}